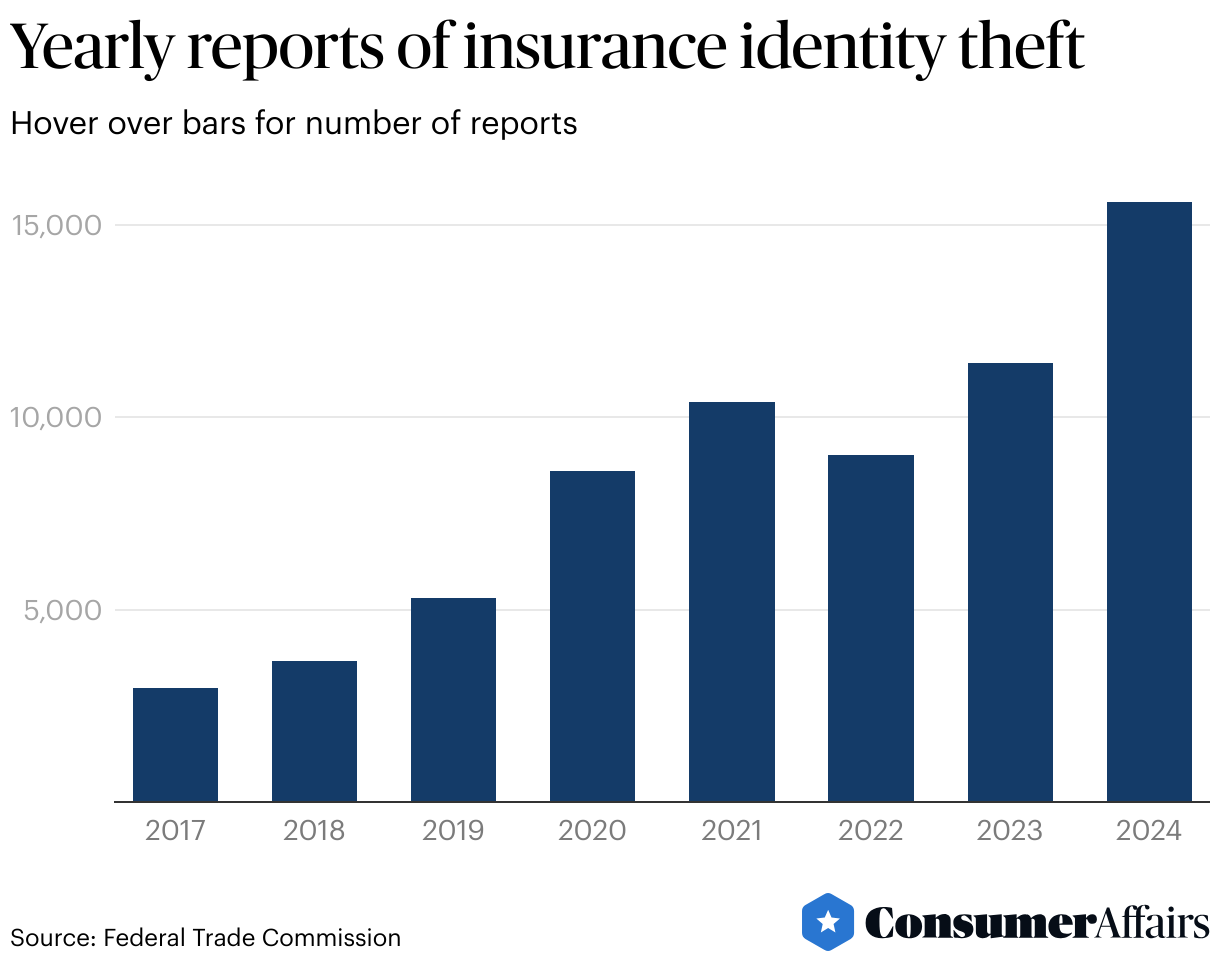

There was a 37% jump in reports in 2024

More consumers are reporting insurance identity theft, a sophisticated fraud that can drive up insurance premiums and cancel policies.

There were 15,587 reports of insurance identity theft in 2024, marking a 37%jump from 2023 and the most reports on record, according to a yearly report from the Federal Trade Commission.

Insurance identity theft also had the biggest increase in reports of any identity theft category in 2024.

The reports don't capture all fraud in the U.S., but represent complaintsfiled to the FTC, other government agencies and organizations such as the Better Business Bureau.

"With insurance becoming harder to obtain for many people, its sadly becoming a tempting target," said Charles L. Moore, a former deputy commander of the United States Cyber Command and now chief military advisor at cybersecurity company Aura, in an interview with ConsumerAffairs.

Insurance identity theft can use someone's personal information to obtain an insurance policy, exploit a current policy or receive medical services under someone else's policy, cybersecurity experts told ConsumerAffairs.

The fraud harmsa customer's insurance records, driving up premiums, damaging their claims history and even leading to a policy cancellation.

And the theft canbeundetected for months and is hard to resolve.

Victims often have to deal with multiple companies, including insurers and health care providers, to correct their personal information and the details of fradulent claims, compared with other forms of identity theft thataccess an established accountor open a new line of credit,said Ian Bednowitz, general manager at Norton LifeLock, in an interview with ConsumerAffairs.

"While other forms of identity theft can also be time consuming to resolve, the remediation process for these cases is generally clearer and more straightforward," said Ian Bednowitz, general manager at Norton LifeLock, in an interview with ConsumerAffairs.

Insurance identity theft is on the rise because the growing amount of personal information available online, weak fraud detection and complex insurance systems,Aura's Moore said.

Artificial intelligence, which can generate convincing text, images and websites, is also making it easier for scammers to ensnare victims and trick companies, he added.

"Scams now look so legitimate that it is difficult to detect them in real time," Mooresaid.

How to avoid insurance identity theft

- Review statements: Check insurance statements to make sure there's nothing unusual, such as premium increases, unauthorized claims or unfamiliar medical providers.

- Strong passwords: Use unique and strong passwords across different platforms.

- Carefully disclose:Be cautious with sharing personal information over the phone, online or through email.

- Report changes:Immediately tell insurers of any changes to your personal information or situation.

- Dispose documents:Carefully destroy or throw away any documents with identifying information, such as medical records and insurance statements.

- Identity theft protection: Various companies offer services that protect people fromidentity theft. ConsumerAffairs has reviews of identity theft services.

Sign up below for The Daily Consumer, our newsletter on the latest consumer news, including recalls, scams, lawsuits and more.

Posted: 2025-03-12 21:53:53