Insurers are hiking costs after more homeowners got dropped

The rising cost of home insurance isn't slowing down at a time of heightened economic uncertainty.

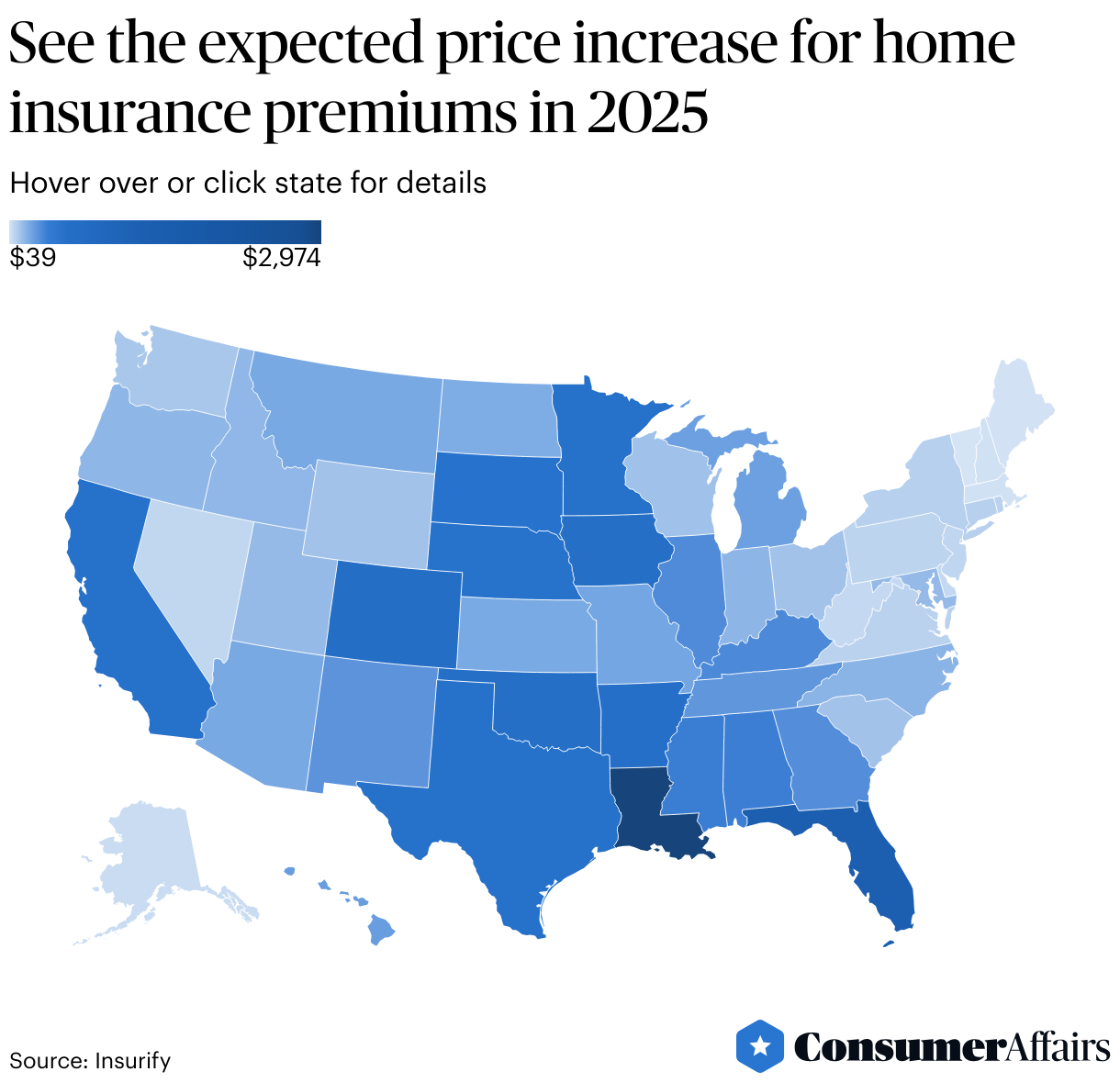

Homeowners in every U.S. state areexpected to seeaverage annual home insurance premiums rise by aslittle as $39 to as much as $2,974, according toa reportfrom insurance-comparison website Insurify.

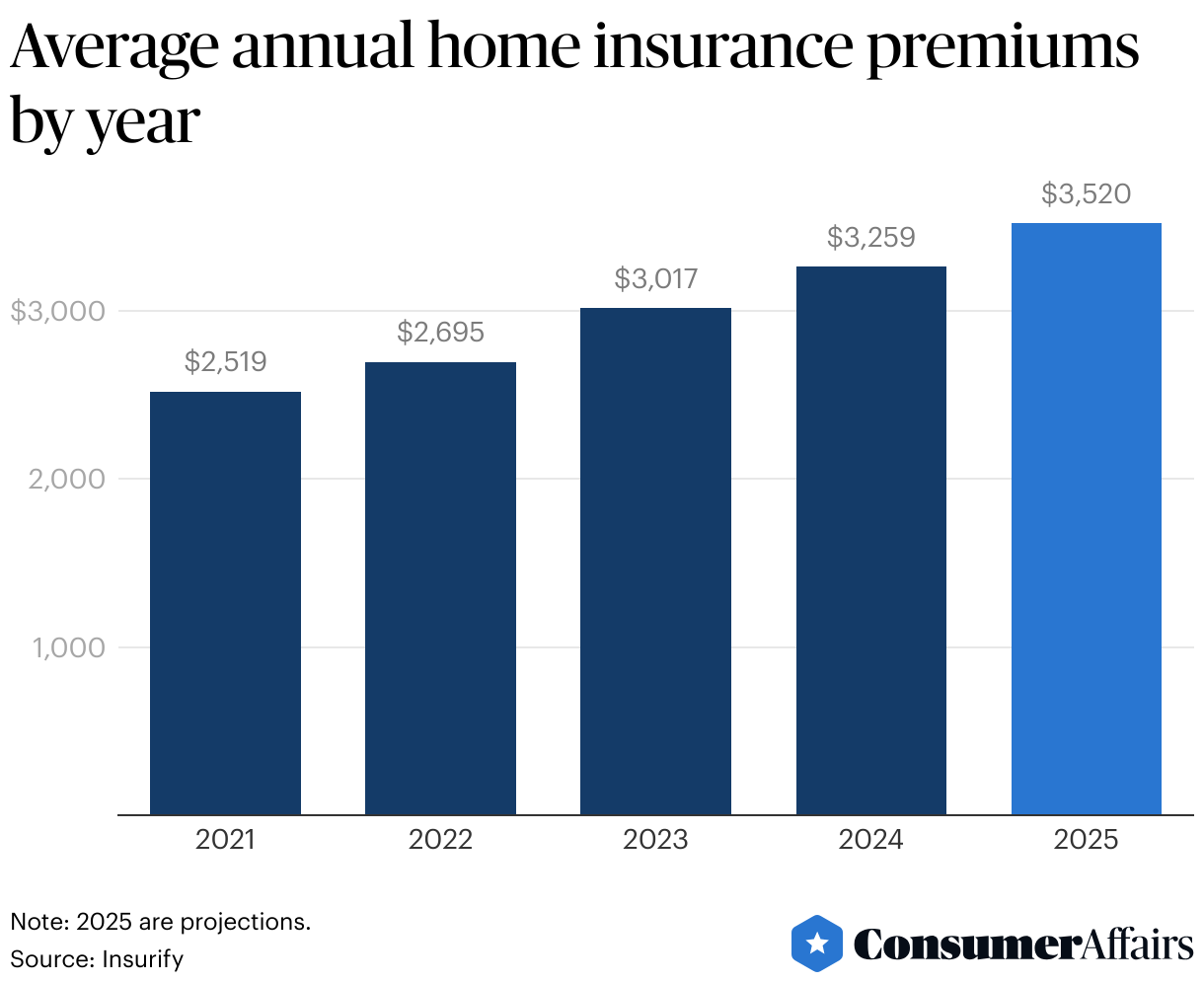

In the U.S. overall, Insurify said it projects average annual home insurance premiums to rise to $3,520 a year in 2025 from $3,259 in 2024, an around8% increase in line with the previous year's 8%.

The latest round of home insurance premium hikes are arriving afterinsurershave raisedprices nearly everywhere and Americans are increasingly getting dropped, worsening the struggle to find affordable housing in the country.

A report from nonprofit Consumer Federation of America found thatinsurers raised homeinsurance premiumsfor single-family homes in 95% of U.S. ZIP codes in 2024 compared with 2021.

And 25% of Americans gotdropped by their home insurer in 2024, up from 19% in 2023, largely because insurers don't want to cover homes in areas more at risk of natural disasters,according to a surveyinsurance comparison-website ValuePenguin.

Where home insurance premiums are costing more

Home insurancecovers monetary damages from unexpected events, including a burst pipe, hailstorm, fire or hurricane, but it generally doesn't cover flooding that homeowners living in Federal Emergency Management Agency-designated (FEMA) areas have to pay for.

Louisiana, where hurricanes have caused more than $115 billion of damagesince 2020, is expected to see the biggest hike in home insurance premiums with $2,974 in 2025, followed by Florida ($1,320), Colorado($646), Iowa ($624) and Oklahoma ($607).

The five states with the smallest expected increases in home insurance premiums are Vermont, with a $39 increase, followed by Maine ($49), Massachusetts ($51), New Hampshire ($48)and Alaska ($47).

Why is home insurance getting more expensive?

Extreme weather fueled by climate change, such as hurricanes in Florida and Louisianaand fires in California,are are a big reason insurers give for raising premiums, Insurify said.

For instance, hailstorms have increased 65% over the last three years in Colorado and aredriving up costs in the state, Insurify said.

But there are other forces than climate change at play.

Reinsurance companies, insurers for insuranceoften based in Bermuda or Europe, operate in an unregulated global market and have raised prices for U.S. insurers for six years in a row, according to Consumer Federation of America.

Insurance is also regulated at the state level and the rules vary in their toughness, with fewer states requiring approval before an insurer can raise premiums.

President Trump's tariffs may raise home insurance premiums even more.

The tariffs are expected to increase the cost onimported consturction materials by $4 billion, according to the National Association of Home Builders, which would make insuring homes costlier.

Insurify said sustained, or long-term tariffs, could mean its projections on home insurance for 2025 are conservative.

Tariffs on imported materials will lead to increased rebuilding costs, which will eventually result in higher insurance premiums, said David Marlett, a professor of insurance at Appalachian State University, in the Insurify report. If the tariffs become entrenched, then their added costs will have to be passed on to the consumer through higher premiums.

How tolowerhomeinsurance premiums

TheInsurance Information Institute has suggestionsto lower homeinsurance bills:

- Shop around:Compare multiple insurers, contact your state insurance department, check consumer guides, speak with insurance agents and use online comparison services to get a good price.

- Raise deductible:Increasing your homeinsurance deductible, or what you pay towards a loss, from typically $500 to $1,000 can lower the amount you pay in monthly premiums.

- Bundle insurance:Buying both your car and home insurance from the same provider can get you a discount.

- Stay with insurer:Keeping the same insurer for several years can get you a discount as a long-term policyholder.

- Improve disaster resilience:You may be able to save on premiums by adding home upgrades such as storm shutters, reinforcing your roof and buying stronger materials.

- Improve security:Installing burglar alarms, dead-bolt locks, smoke detectors and fire sprinklerscan lower your monthly homeoinsurance premiums.

Sign up below for The Daily Consumer, our newsletter on the latest consumer news, including recalls, scams, lawsuits and more.

Posted: 2025-04-08 13:01:05