States attracting young homebuyers have lower prices compared with income

Key takeaways:

- Minnesota, West Virginia and Michigan are among the best states for young people to buy a home, based on homeowernship rates and income by age.

- Hawaii, New York and California are some ofthe worst states for young people to buy a home.

- Baby boomers overtook millennials for homebuying in 2024, showing thatthehomeownership gap isn't improving.

Young people are buying homes in more affordable states away from urban centers.

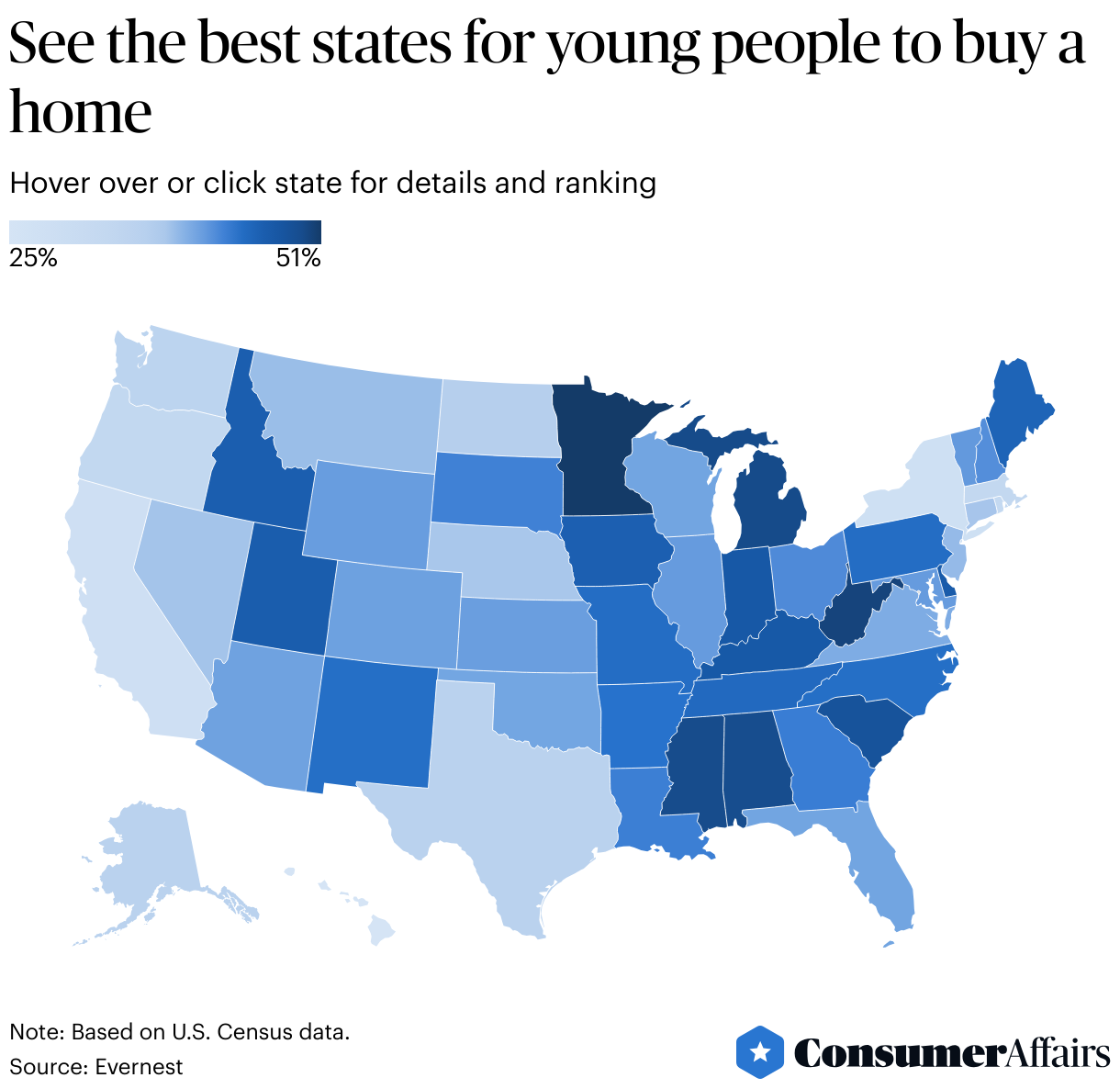

Non-coastal states with lower costs of living such as Minnesota, West Virginia and Michigan are among the best states for young people to buy a home,according to a report from property-management companyEvernest, which analyzed the latest U.S. Census homeownership data for people under 35 years old.

Minnesota, with a homeownership share of 51% among peopleaged 35 and under, is the best state for young people to buy a home.

"With over half of Minnesotans under 35 achieving homeownership nearly double the rate in high-cost coastal markets we're witnessing young Americans prioritize financial stability and space over traditional urban amenities," Evernest said.

Minnesota is followed by West Virginia (50%), Michigan (49%),Mississippi (49%) andAlabama (49%) in the rest of the top five best states for young people to buy a home.

States attracting younger homebuyers often have lower home prices compared to income, such as Minnesota with an average home price of $323,437 and average income of $94,870 among people aged 35 and under.

On the other hand, the worst state for young people to buy a home was Hawaii, with a homeownership share of 25% among people aged 35 and under.

Young people in Hawaii had an average income of $94,200, which is below Minnesota, and an average home price of $829,941.

The other five worst states for young people to buy a home are New York (28%), California (28%), Rhode Island (32%) andMassachusetts (33%).

The homeownershipgap among generations

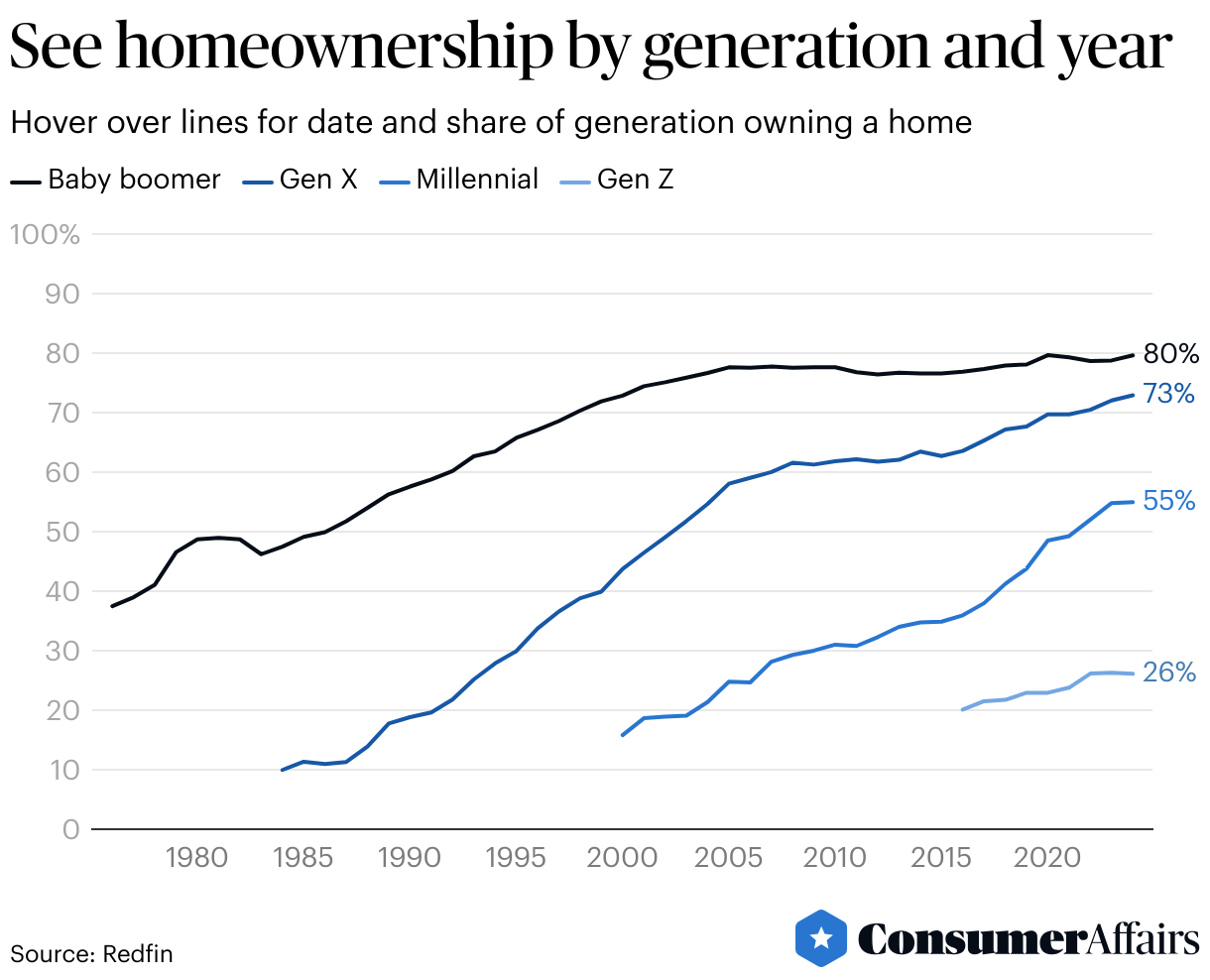

Younger people may want to consider more affordable states for buying a home after the struggle for homeownership among generations has shown little improvement.

Homeownership rates among millennials and Gen Z people flatlined in 2024 compared with 2023 and 2022, according to a report from real-estate brokerage Redfin.

Part of the reason is because some young people are choosing to rent because they can't afford to buy a home, Redfin Chief Economist Daryl Fairweather said in the report.

A median priced home now requires an income $52,473 higher than renting a median priced home in 2025, which is up from $46,808 in 2024, Redfin said.

"Buying a home is still typically a good financial investment, but for young people who dont have the desire or means to do so, there are other viable investments that, unlike buying a home, dont require a huge down payment," Fairweather said.

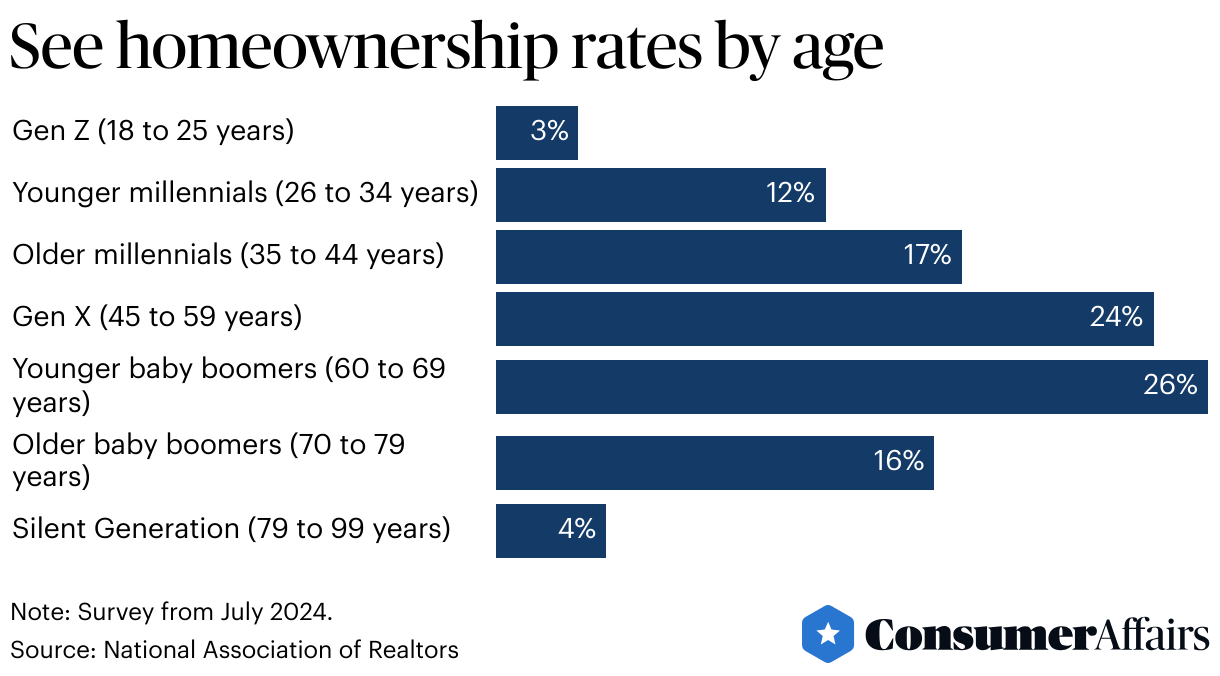

And baby boomers recently overtook millennials for homebuying in 2024, with a 42% share compared with 29% among millennials after the younger generationfell from 38% in 2023, according to a survey by the National Association of Realtors.

"In a plot twist, baby boomers have overtaken millennials the largest U.S. population to become the top generation of home buyers," said Jessica Lautz, NAR deputy chief economist and vice president of research, in a statement. "What's striking is that half of older boomers and two out of five younger boomers are purchasing homes entirely with cash, bypassing financing altogether."

People aged 60 to 99 years also accounted for 58% of home sellers, NAR said.

The generational gap in homeownership is stoking frustration among younger people in the economy,said Amy Nixon, a housing and economic analyst, ina poston X, formerly Twitter.

"Until this is corrected, populism rages on," she said."Imagine the outrage if young people made a run on walkers, wheelchairs, or diabetes medication, then colluded in agreement to only sell them to old people who really need them for a 300% markup."

Sign up below for The Daily Consumer, our newsletter on the latest consumer news, including recalls, scams, lawsuits and more.

Posted: 2025-04-14 21:42:04