North Dakota has been attracting renters from other states in recent years

Key takeaways:

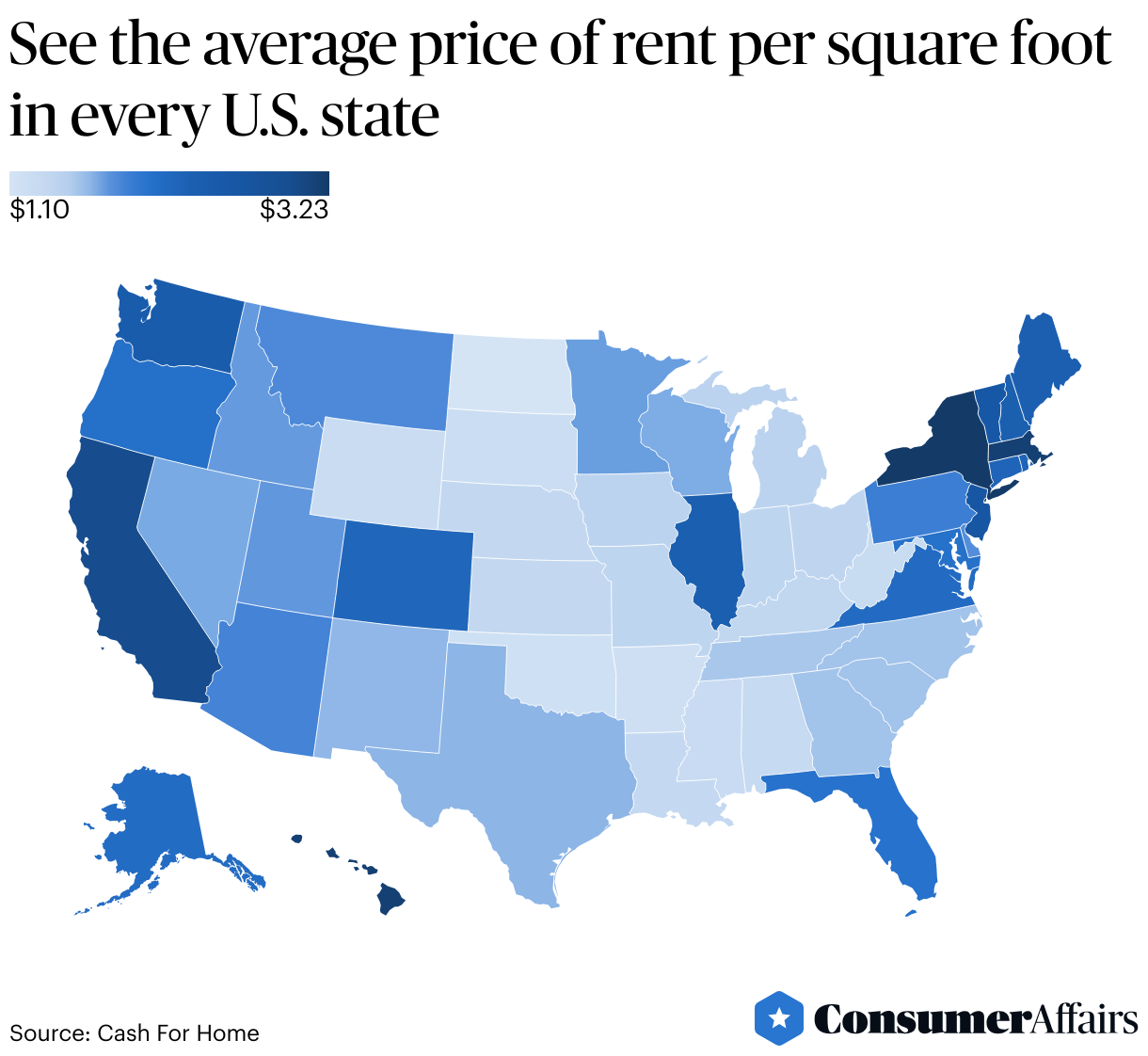

- North Dakota, Oklahomaand Arkansasare the three best states for price of rent per square foot.

- New York, Massachusetts and Hawaiiare the three worst states for price of rent per square foot.

- States in the Midwest, South and West typically have better rent prices forthe cost of space.

It's no secretrenters end uppaying a lot more for less space across the country.

But some states have much lower rents based on the cost of space.

Rent prices per square foot variedwidely from as little as $1.10 a square foot to as much as $3.23 amongstates, according to data provided to ConsumerAffairs by Cash For Home, which analyzed the average rent price per square foot by state.

North Dakota is the best state for renters by price per square foot, costing $1.10 a square foot, followed by Oklahoma ($1.19), Arkansas ($1.20), South Dakota ($1.25) and Wyoming ($1.27).

North Dakotaoutpaced the rest of the U.S. in domestic migrationin 2023, the latest year of data from the U.S. Census, in part because of its low cost of living and and economic opportunity attracting Americans from other states, ConsumerAffairs previously reported.

"In states like New York, youre paying top dollar for less room," Nathan Richardson, real estate expert and founder of Cash For Home, told ConsumerAffairs. "In places like North Dakota, the same money gets you space to live, growand breathe."

The worst state for price of rent per square foot is New York, costing $3.23 a squarefoot. The other five worst states are Massachusetts ($3.16), Hawaii ($3.16), California ($2.99) and New Jersey ($2.64).

"Affordability in real estate isnt just about monthly rentit's about what you're getting in return," he said.

Cost per square foot is an often overlooked figure in the rental market that gives a more accurate picture of value when comparing across locations, he said.

"In lower-density areas, you're not only getting more space for your dollar, but often a better quality of life: less congestion, more privacy, and room to grow, literally and figuratively," Richardson said. "With remote and hybrid work becoming the norm, renters are no longer tied to high-cost urban centres, making states like North Dakota or Arkansas even more appealing."

Sign up below for The Daily Consumer, our newsletter on the latest consumer news, including recalls, scams, lawsuits and more.

Posted: 2025-04-22 11:17:25