Hurricane Helene recently took Florida to the top spot for natural-disaster losses

Key takeaways:

- Texas, Georgia and Illinoisare the three worst states for natural disasters.

- Hawaii, Alaskaand Maineare the three best states for natural disasters.

- Natural disaster frequencyand losses are worsening, which is hurting homeowners.

Natural disasters are getting worse and residents of some states are suffering much more, raising concerns about buying homes in riskier areas and getting home insurance, according to a ConsumerAffairs analysis ofdata spanning 1980 to 2024fromthe National Oceanic and Atmospheric Administration.

The figures, updated April 8, 2025, include droughts, flooding, freezes, severe storms, tropical cyclones, wildfires and winter storms.

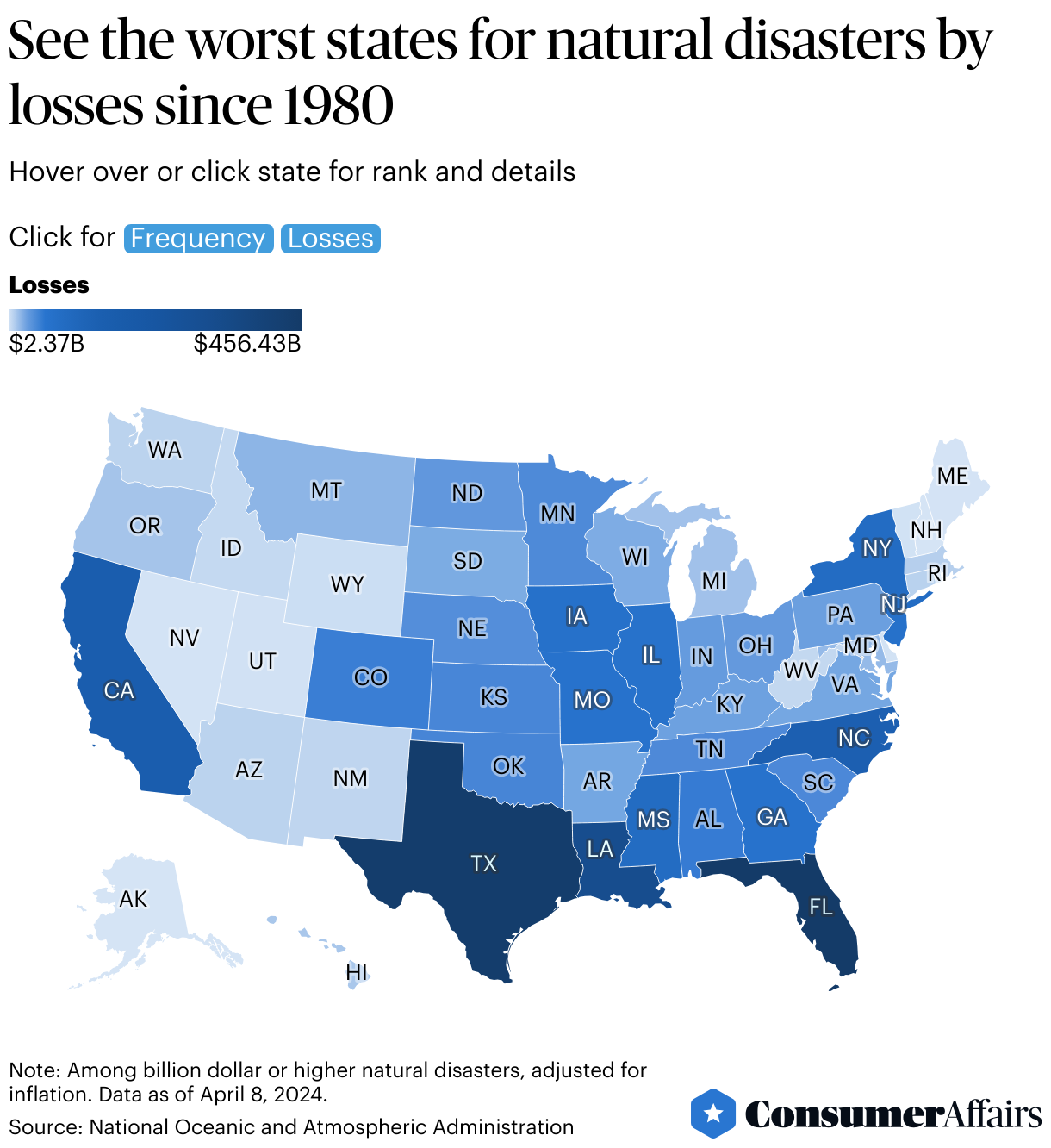

Texas is the worst state for natural disasters, with 190natural disasters costing a billion dollars or more since 1980 through 2024, followed by Georgia (134), Illinois (128), North Carolina (121)and Missouri (120).

Florida is the worst state for natural-disaster monetary losses, with 94 natural disasters costing around$456.4billion since 1980, followed by Texas ($440.6 billion), Louisiana ($318.1 billion), California ($156.8 billion)and North Carolina ($137.2 billion).

In mid-2024, Texas was the worst state for natural disasters in terms of dollarlosses, but that year's Hurricane Helene helped boostFlorida to the top spot.

On the other hand, Hawaiiwas the best state for natural disasters, with only twonatural disasters since 1980 through 2024, followed by Alaska (8), Maine (19), Vermont (19)and New Hampshire (21).

New Hampshire was the best state for natural-disaster losses, with 21 natural diasters costingaround $236.9billion since 1980, followed by Alaska($237.6 billion), Maine ($265.6 billion), Nevada ($292.8 billion)and Rhode Island ($300.9 billion).

Are more natural disasters happening?

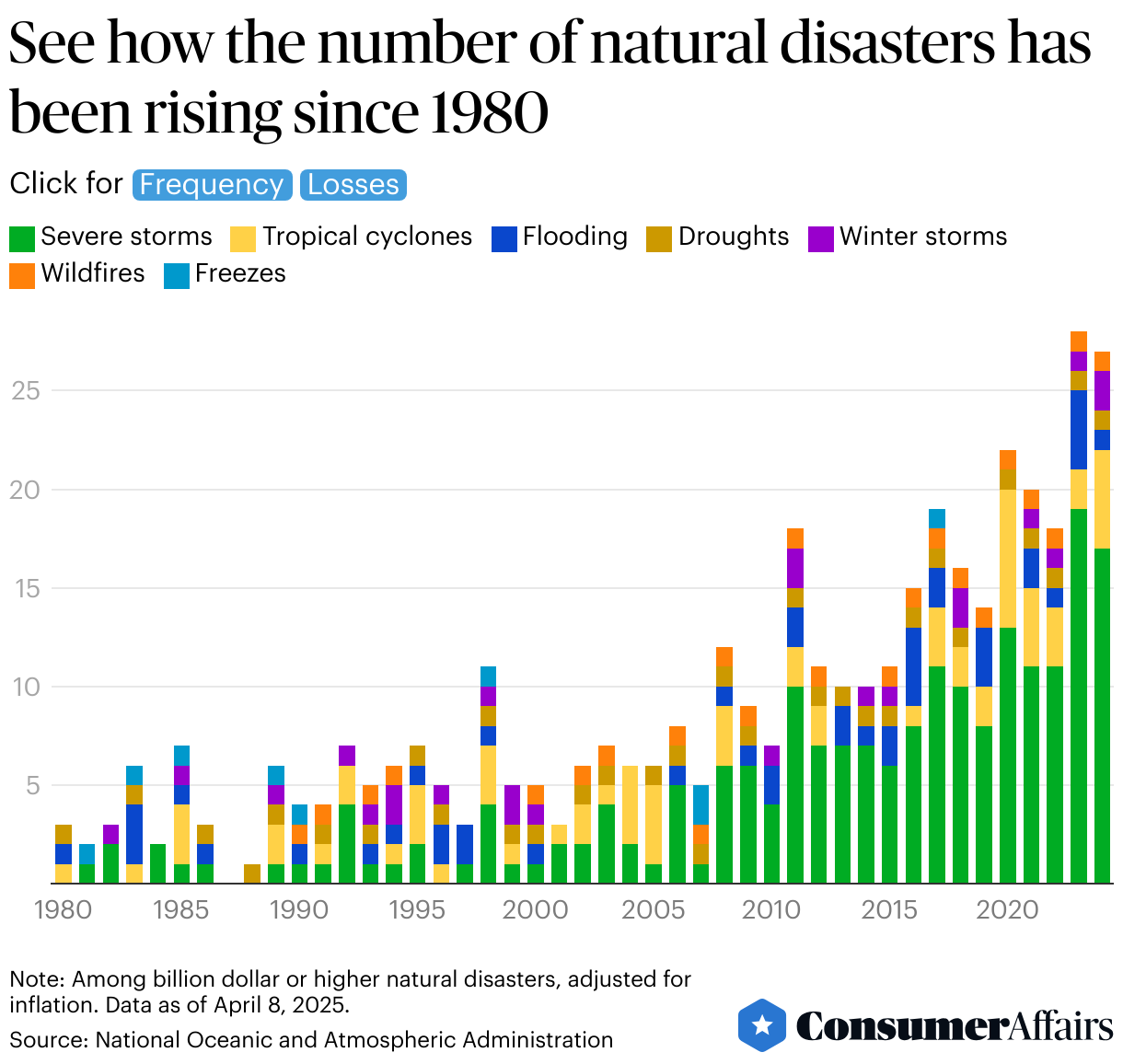

In recent years, more natural disasters have been happening and losses have ballooned.

Over 10 years from 2015through 2024, there were 190natural disasters, nearly doubling from 96over the previous 10-year period.

Losses from natural disasters totaled more than $1.42 trillionover the last 10 years of data, also nearly doubling from $769.6 billionover the previous 10 years.

Tropical cyclones, the strongest of which are hurricanes, have accounted for the biggest share of losses in recent years, despite being much less frequent than other severe storms.

Climate scientists say global warming, spurred by industrial activity releasing greenhouse-gas emissions, is making natural disasters more frequent and more destructive.

In 2025, NOAA said there are potential billion-dollar natural disasters it still hasn't added to its data, including the Los Angeles fires, March's severe weather in the South and East, March'stornado outbreak in the Central and Southeastern U.S. and April's flooding and tornado outbreak in the Midwest and South.

How are natural disasters affecting housing?

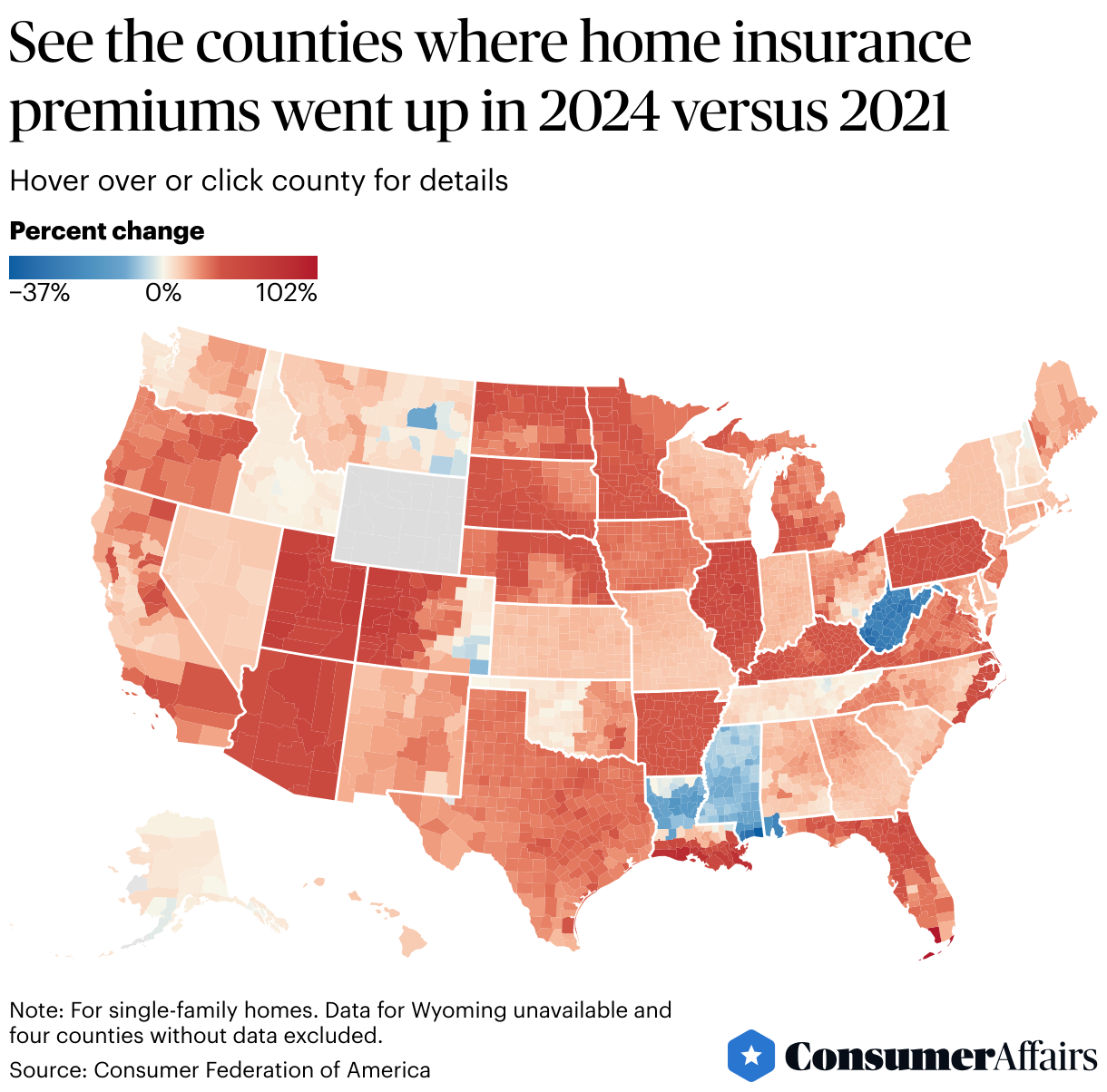

Natural disasters are making housing less affordable, in large part because they are causing insurers to charge more for home insurance.

Home insurance is costing more nearly everywhere in the U.S. now: Insurers raised homeowners insurance premiums for single-family homes in 95% of U.S. ZIP codes in 2024 compared with 2021, according to a study from nonprofit Consumer Federation of America.

For instance, hailstorms have increased 65% over the last three years in Colorado and are driving up home insurance costs in the state.

"While hurricanes and wildfires often attract most attention, a rise in extreme weather events is impacting almost all parts of the country, including many states in the Midwest," said the authors of the Consumer Federation of American study.

Sign up below for The Daily Consumer, our newsletter on the latest consumer news, including recalls, scams, lawsuits and more.

Posted: 2025-04-24 11:22:05