Shorter mortgage terms and bigger down payments can lower housing costs

Key takeaways

- Iowa, West Virginia and Kansas are the three best states for spending less income on owning a home in 2025.

- For spending less income on renting, Kansas, Iowa and Wyoming are the three best states.

- Both homeowners and renters should strategize a budget and aim to spend no more than 30% of their yearly income on housing.

Budgeting how much of your income is spent on amortgage or rent is critical when finding affordable housing.

States in the West and Northeast of the U.S. generally had more affordable housing, while states in the Midwest and South were less so, according to financial-advice websiteWalletHub, which analyzed the costs of rent, mortgages and energy compared with median incomes.

Iowa was the best state for spending less income on owning a home, costing nearly 19% of yearly income, followed by West Virginia (20%), Kansas (20%), Nebraska (20%) and Ohio (20%).

Financial planners recommend spending no more than 30% of income on housing, before taxes and deductions.

"Setting a clear, realistic budget from the start is one of the smartest moves you can make," Chip Lupo, analyst at WalletHub, told ConsumerAffairs.

The good news is costs for owning a home, including mortgage and energy,took less than 30% of typical incomes in 37 states, according to the WalletHub data, which showsthere are many pockets of affordable housing across the country,

On the other hand, Hawaiiwas the worst state for how much income went to owning a home, costing nearly 47% of income. The other five worst states are California (46%), Oregon (36%), Nevada (35%) and Washington (35%).

The rankinghighlights pitfalls and opportunities in affordable housing among states after the cost to buy a home has outpaced inflation, pricing out would-be homebuyers from the market.

"With home prices rising and interest rates bouncing back from historic lows, buying a home today requires some strategic planning," Lupo said. "So to keep control of your finances, consider a shorter mortgage term, work on improving your creditand strive for a large down payment to reduce interest costs."

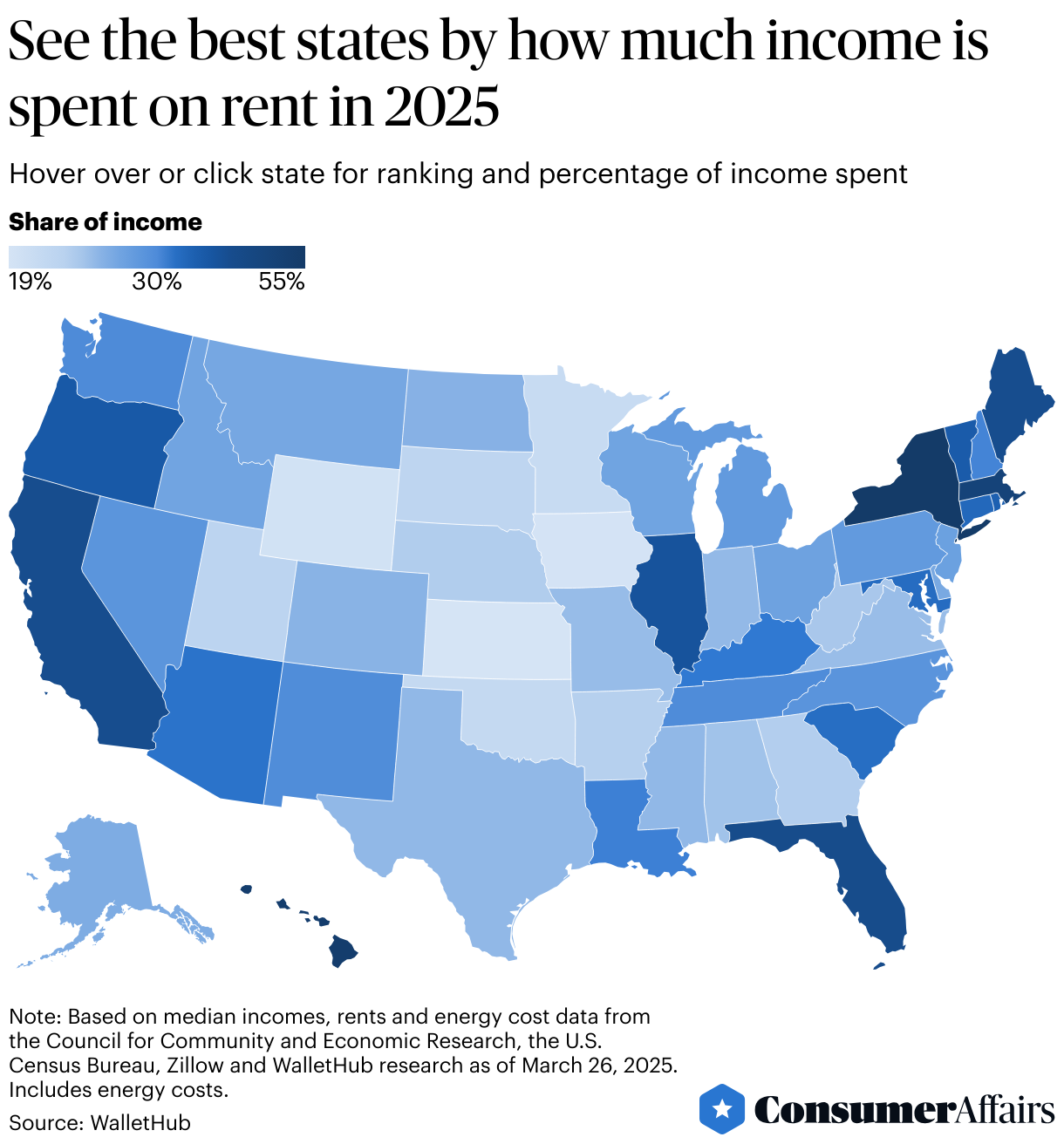

What were the best states for affordable rent?

Rent cost less than 30% of yearly income, the recommended level for affordable housing, in 32 states, according to WalletHub.

The best state for spending less income on rent is Kansas, costing around 19% of a typical yearly income, followed by Iowa (19%), Wyoming (20%), Minnesota (21%) and Oklahoma (22%).

The worst state for spending less income on rent is New York, costing nearly 55% of income. The other five worst states are Hawaii (53%), Massachusetts (49%), Florida (43%) and Maine (42%).

Hawaii andMassachusetts both ranked in the top 10 worst states for homeowners and renters.

Lupo said that the real-estate market is putting pressure on renters, too. He saidrent can cost more than 40% of yearly income instates with expensive homes such as New York and Florida.

Energy bills should also be top of mind for both homeowners and renters, he said.

"Remember, housing costs are more than just mortgage or rent," Lupo said, pointing to how Hawaii hassome of the highest home energy costs in the country. "Cutting down on water, heatand electricity use can make a noticeable difference in your monthly expenses, whether you own or rent."

Sign up below for The Daily Consumer, our newsletter on the latest consumer news, including recalls, scams, lawsuits and more.

Posted: 2025-04-24 11:16:40