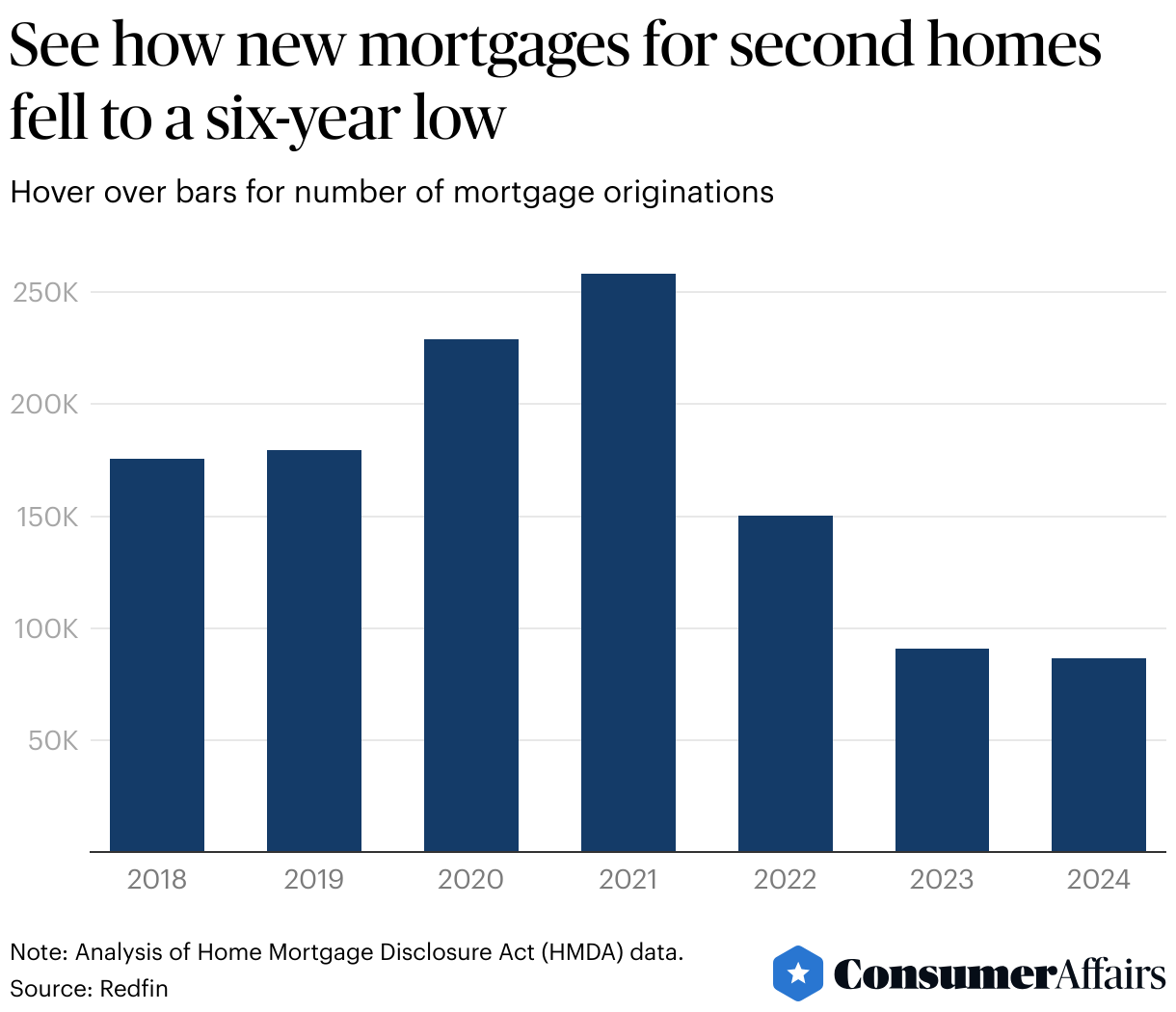

New mortgages for second homes, often thought of as vacation homes, fell to a 6-year low in 2024.

High interest rates and home insurance costs are keeping Americans from buying second homes, especially in Florida where demand has fallen the fastest.

West Palm Beach, New Brunswickand Riversidehad the highest shares of second-home mortgages.

Americans have been increasingly hesistant to buy a second home, following high mortgage rates and home insurance costs.

There were 86,604 mortgage originations for second homes in 2024, the lowest level in six years, acccording to an analysis by real-estate brokerage Redfin, which reviewedHome Mortgage Disclosure Act (HMDA) data.

Redfin said second-home mortgages accounted for just 2.6% of all new mortgages in 2024, the lowest share on record, and down from a peak of 5% in 2020.

Most people arent buying vacation homes at all because mortgage rates and insurance costs especially for waterfront homes and condos have skyrocketed,"said Lindsay Garcia, a Redfin Premier agent in Fourt Lauderdale, Fla., in a statement."Plus, people know theyre unlikely to earn much revenue from listing on Airbnb now that occupancy rates are down.

Some people are still buying homes and they are typicallyrich, middle aged and white, Redfin said.

While some wealthy cash buyers are still purchasing second homes, they are much more likely to make a low-ball offer or request concessions than they used to be," Garcia said.

Where is demand for second homes falling?

Florida is seeing the fastest decline in second home purchases, despite remaining one of the most popular destinations for vacation homes, Redfin said.

Redfin said the Sunshine State is suffering a decline in second-home purchases largely because of soaring home insurance costs, property-tax costs and homeowners association (HOA) fees.

Miamihad the biggest decline in second-home mortgage originations among the 50 most-populous metros, with a 32.2% drop in 2024 from 2023, followed by Orlando (-28.4%), Fort Lauderdale (-28%), West Palm Beach (-23.7%) and Tampa (-20.9%).

Still, West Palm Beach remained the most popular metro for second homes, accounting for 5.6% of new mortgages in 2024, followed by New Brunswick, N.J. (4.2%), Riverside, Calif. (3.5%), Las Vegas, Nev. (3.2%) and Nassau County, N.Y. (3%) in the rest of the top five.

Broadly, mortgages for second homesfell in 30 ofof the 50 most-populous U.S. metros, but increased the most in Detroit, Mich. (+26%), San Francisco, Calif. (+17%) and San Jose, Calif (+15.9%), Redfin said.

The least popular metro for second homes was Montgomery County, Pa., with 0.4% of new mortgages in 2024, followed by Oakland, Calif. (0.5%), Forth Worth, Texas (0.6%) and Detroit, Mich. (0.6%) in the rest of the bottom five.

Sign up below for The Daily Consumer, our newsletter on the latest consumer news, including recalls, scams, lawsuits and more.

Housing and insurance costs remain stubbornly high, keeping monthly bills elevated even as overall inflation cools.

Food prices have stopped rising rapidly but are still far above pre-pandemic levels, stretching household budgets.

Everyday services from utilities to car repairs continue to climb, quietly eroding purchasing power.

Inflation has been relatively tame for several months, a welcome change after years of rapid price increases that rattled consumers and policymakers alike. Official measures show price growth has slowed across much of the economy, and in some categories, increases have nearly stalled.

Yet for many Americans, relief feels elusive. The reason is increasingly clear: while inflation may be low, affordability is not improving at the same pace.

Inflation measures how quickly prices are rising, not whether prices are high to begin with. After several years of sharp increases, many essentials remain far more expensive than they were before the pandemic. Even modest price growth today is being layered on top of already elevated costs, leaving households feeling financially squeezed.

Housing leads the pain

Compounding the price pain is the fact that some important spending categories remain elevated. For example, housing-related expenses remain the biggest source of strain.

Rent increases have slowed nationally, but rents are still significantly higher than just a few years ago. Homeownership has become even more challenging as elevated mortgage rates push monthly payments out of reach for many buyers.

Property taxes, homeowners association fees, and especially insurance premiums are adding to the burden. Home and auto insurance costs have surged due to higher repair costs, extreme weather losses, and increased claims, hitting consumers regardless of whether they rent or own.

Food prices: Stabilized, not reversed

Grocery prices are no longer climbing at the dizzying pace seen in 2022 and early 2023, but they also havent meaningfully fallen. Shoppers still face higher prices for staples such as meat, dairy, and packaged foods compared with pre-pandemic norms.

For families living paycheck to paycheck, this matters more than the inflation rate itself. Even small weekly increases accumulate over time, forcing tradeoffs like buying cheaper brands, cutting back on fresh foods, or relying more heavily on credit.

Another key pressure point is services the costs that are hardest to avoid or substitute. Utilities, medical services, childcare, car repairs, and personal services continue to rise steadily. Labor costs, which make up a large share of service prices, have remained elevated, and those increases are often passed directly to consumers.

Unlike goods such as electronics or furniture, services rarely get cheaper. Once prices rise, they tend to stay high, locking in affordability challenges even when overall inflation appears under control.

Why it feels worse than the numbers suggest

Wages have risen, but not always fast enough or evenly enough to offset higher living costs. Many households are also dealing with depleted savings after years of inflation, making them more sensitive to everyday expenses. Credit card balances are higher, and interest rates mean carrying debt is more expensive than it used to be.

As a result, consumers may hear that inflation is low and wonder why their finances dont reflect that improvement. The answer lies in the difference between slowing price growth and genuinely lower prices a gap that remains wide.

Unless incomes rise faster or key categories like housing, insurance, and services begin to ease, affordability is likely to remain a dominant concern. Inflation may no longer be the headline economic problem, but for many households, the cost of simply getting by is still uncomfortably high.

Grocery-store ground roast coffee averaged $9.14/lb in September, up from $6.47/lb a year earlier a 41% jump thats showing up on receipts fast

Weather-driven supply hits + a surge in wholesale arabica prices pushed costs up, and tariffs added fuel at the worst time. Even with tariff rollbacks, shelf prices usually lag

Do quick cost-per-cup math (home brew is still far cheaper), buy extra duringsales and freeze abag, and watch the unit price for shrinkflation

If your normal bag of ground coffee is starting to feel like more of a splurge item, youre not imagining things. Federal pricing data shows supermarket coffee is up sharply. As of September, a pound of ground roast coffee averaged about $9.14, up from $6.47 a year earlier. Thats a whopping 41% jump in just 12 months.

Whats behind the coffee spike

Weather problems tightened supply

Coffee is considered a picky crop, and production disruptions like bad weather in the major growing regions, can affect supply quickly. When harvests come up short, roasters and importers scramble, and so costs naturally climb.

Wholesale coffee prices surged

In early 2025, arabica coffee futures pushed above $4.30 per pound at one point, with traders pointing to limited availability and even some panic in the market.

Think of futures prices as a benchmark for what many buyers pay for their beans. So, when you see a big jump like we saw earlier this year, it tends to show up down the road at grocery stores and coffee chains.

Tariffs added cost at the worst time

In April 2025, the U.S. imposed a 10% base tariff on many imports and layered on additional duties that varied by country. These included goods the U.S. doesnt really produce domestically, like coffee.

In mid-November, the White House rolled back tariffs on more than 200 food products, including coffee, with the changes taking effect retroactively.

The National Coffee Association said removing reciprocal tariffs should ease cost pressures for coffee drinkers and the businesses that depend on imports.

Then, on Nov. 21, Reuters reported the administration removed a remaining 40% tariff on many Brazilian agricultural imports, including green coffee beans. This was a big deal because Brazil supplies about a third of U.S. coffee beans.

Why prices may not drop overnight

Even if the tariff line item disappears, retail prices usually lag behind for a while. This is because roasters buy beans months ahead, retailers adjust prices in cycles, and brands rarely cut shelf prices the moment their costs ease.

Coffee shops have nudged prices up, too. Toasts menu data shows the median price of a regular coffee on restaurant menus was $3.57 in October 2025, up 3.2% from a year earlier.

The coffee price playbook for shoppers

Here are five money moves that will help you saveon your next cup:

1. Do the cost-per-cup math (its sobering)

A pound of coffee can make roughly 22 standard 12-ounce cups at home if youre using about 20g per cup.

At $9.14 per pound, thats about 42 cents per cup before milk and sugar versus about $3.50 for a basic caf coffee. I know its boring and you've probably heard it a hundred times, but brew your own cup of joe at home and save big.

2. Buy on deal, then bank the savings

When your coffee go-to brand hits a real sale, grab two bags and freeze one. Sealed coffee holds up well in the freezer, and buying at the low point beats paying whatever the shelf tag says next week.

3. Use store brands strategically

If your go-to brand jumped 30% to 50%, a private-label or club-store option can bring your cost per cup back to earth. Test one bag before you commit, then buy larger sizes when you find a winner.

4. Stop paying the add-on tax at coffee shops

If youre buying out of habit, keep the ritual but downgrade the order: drip instead of latte, fewer pumps, skip the foam. Most of the coffee inflation you feel at cafs comes from extras.

5. Watch for shrinkflation

Coffee brands love to keep the sticker price steady and quietly reduce the ounces. Always compare the unit price (per ounce or per pound) on the shelf tag, not the number printed on the bag.

Plaintiffs allege Pepsi and Walmart coordinated pricing to inflate soft drink costs nationwide

Lawsuit claims Walmart received preferential wholesale prices while rivals paid more

Case follows FTCs decision to drop a Robinson-Patman Act lawsuit against Pepsi

PepsiCo and Walmart have been accused in a new consumer class action lawsuit of orchestrating a decade-long price-fixing scheme that allegedly inflated the cost of Pepsi soft drinks at retailers across the United States.

The lawsuit, filed Monday in federal court in New York, alleges the two companies entered into an unlawful agreement that gave Walmart preferential wholesale pricing on Pepsi products while forcing competing retailers to pay higher prices. Plaintiffs say the arrangement violated federal antitrust law and ultimately harmed consumers by driving up retail prices outside Walmart stores.

Allegations of preferential pricing

According to the complaint, Pepsi offered Walmart favorable pricing and other incentives designed to maintain a consistent price gap that allowed the retail giant to sell Pepsi products at lower prices than its competitors. To preserve that gap, the lawsuit alleges, Pepsi raised wholesale prices charged to other retailers, effectively shifting higher costs onto consumers who did not shop at Walmart.

The plaintiffs contend that the pricing arrangement discouraged competition among retailers and insulated Walmart from price pressure, while smaller chains and independent stores were left at a disadvantage.

Link to prior FTC enforcement

The consumer lawsuit follows the Federal Trade Commissions decision in May to drop a case brought during President Joe Bidens administration accusing Pepsi of violating the Robinson-Patman Act, a 1936 law aimed at preventing discriminatory pricing practices that favor large buyers over smaller competitors.

The FTCs case named Pepsi as the sole defendant and did not include Walmart. In that matter, the agency alleged Pepsi had offered preferential pricing and promotional benefits to Walmart while denying similar terms to other retailers. Pepsi denied wrongdoing, and the case was later withdrawn by the agency.

Plaintiffs in the new lawsuit cite similar conduct, arguing that Pepsis alleged preferential treatment of Walmart went beyond lawful discounting and crossed into anticompetitive coordination.

Proposed nationwide consumer class

The proposed class includes all U.S. consumers who purchased Pepsi soft drinks from non-Walmart retailers since January 2015. The lawsuit seeks damages and other relief on behalf of consumers who allegedly paid higher prices as a result of the claimed scheme.

Pepsi and Walmart have not yet publicly responded to the new lawsuit. The case adds to ongoing scrutiny of pricing practices between major manufacturers and dominant retailers, particularly as regulators and private plaintiffs examine whether discount arrangements unlawfully harm competition and consumers.

Victims trafficked through Backpage or CityXGuide may be eligible for compensation from a $200 million DOJ fund

The program covers financial losses such as medical care, counseling, and lost income

Survivors must apply by March 31, 2026

Federal authorities are urging people who were sex trafficked through the classified advertising sites Backpage and CityXGuide to apply for compensation through a special Department of Justice program before a March 31, 2026, deadline.

The FBI and DOJ announced the launch of the Backpage Compensation Program in July, following the forfeiture of roughly $200 million in assets connected to the sites. The money is intended to compensate trafficking survivors for eligible financial losses suffered between 2004 and 2020, including medical expenses, counseling costs, and lost income.

Officials say the effort is focused on ensuring that as much of the forfeited money as possible reaches survivors.

The goal is to return as much of the $200 million as possible to victims of trafficking, said Desirae Tolhurst, a special agent with the FBIs Phoenix Field Office who led the Backpage investigation.

Documentation is key to claims

Tolhurst said documentation is the most critical element in securing compensation, but acknowledged that gathering records can be challenging for survivors.

Medical records, receipts, emails, and even copies or screenshots of online advertisements can help support claims, she said. However, aliases, prepaid burner phones, and fake contact information were common in trafficking situations, making verification more difficult.

So its not as straightforward as you might think, Tolhurst said.

Because of those challenges, federal agencies have expanded outreach efforts, including digital media campaigns and partnerships with more than 100 nonprofit organizations and service providers, to help victims understand the program and navigate the application process.

NCMEC connects survivors with free legal help

One of those partners is the National Center for Missing & Exploited Children, which has created a Backpage Survivor Remission Network to help eligible individuals pursue compensation.

NCMEC launched its outreach effort on Sept. 4, and by early December 2025 had connected more than 370 trafficking survivors with lawyers from about 35 national law firms providing pro bono services, according to the organization.

Weve been able to elevate our partnership with law firms, medical health clinicians, and so many others and bring them into the fold to support the larger good of this compensation process, said Yiota Souras, NCMECs chief legal officer.

Survivors are allowed to file petitions on their own, but Souras emphasized that free assistance is available.

I certainly think its important to know that people can complete petitions on their own and submit them, she said. But I think its also important to know there are free resources available to help a trusted partner to walk alongside survivors and help them through this.

Background on Backpage and CityXGuide

Backpage.com was once one of the largest online classified advertising platforms in the United States. From 2004 until its seizure in 2018, federal prosecutors say the site was widely used to facilitate commercial sex and sex trafficking, including the trafficking of minors.

The federal government seized Backpage.com in April 2018 and later brought criminal charges and civil forfeiture actions against its owners and operators. Several were convicted of crimes including conspiring to facilitate unlawful commercial sex and money laundering and were sentenced to federal prison.

CityXGuide later emerged as a successor site and operated until June 2020, when it was also shut down.

Data recovered from Backpages databases dates back to 2004, but officials note that its reliability varies because ads often used aliases, obscured images, and outdated phone numbers.

Who is eligible and how to apply

Individuals may qualify for compensation if they were trafficked through advertisements posted on:

Backpage.com between Jan. 1, 2004, and April 6, 2018

CityXGuide between April 8, 2018, and June 19, 2020

Victims may file petitions themselves, through a representative, or through the estate of a victim who has died.

More information about eligibility and the application process is available at BackpageRemission.com.

Price match identical items, then hunt yellow tags: .06 = clearance, .03 = final markdown (check the tag date)

Do a 10-second app check in the aisle. If its cheaper online, buy online and choose store pickup

Use the money-saver lane: check Daily Deals, save receipts with free Pro Xtra, and rent or buy retired rental tools instead of buying new

The Home Depot is one of those stores where its easy to overspend because a tool often looks like a deal and you think you cant live without it. The trick to saving at Home Depot isnt about a being a coupon wizard or DIY expert. Its all about knowing a few policies + pricing secrets + timing tricks that consistently cut your total bill.

Here are 7 Home Depot hacks that will change the way you shop in the land of orange aprons moving forward.

Get a Home Depot price match

Home Depots price-match policy is pretty clear, as long as the item is identical (same brand/model/size), and the competitor has it in-stock, theyll match the lower price.

Heres how to make it happen in 60 seconds:

Pull up the competitors product page on your phone.

Zoom in on the model number and the in-stock message to make sure it qualifies.

Bring the exact Home Depot listing to an employee and theyll verify it and get you the lower price.

Pro tip: Keep in mind that most price-match attempts fail because people show similar items. Home Depot tells you up front that the item must be identical, down to the color.

Learn to decode the Home Depot price tag

Over the years Ive had several friendly Home Depot employees help me decode their price tags. Information you can use to figure out how good of a deal youre actually getting in-store.

Heres what you need to know:

Prices ending in .06 on a yellow price sticker: An employee who handles price changes at his store told me a yellow tag with a price ending in .06 is on clearance and typically has about six weeks before the next markdown.

Prices ending in .03 on a yellow price sticker: The employee also told me that if an item still hasnt sold after that 6-week window, it may drop again to an ending price of .03. Thats basically the last call price. In his experience, once an item reaches .03, it has about three weeks before its liquidated and removed for good.

Pro tip: Always check the date printed at the bottom of the yellow tag. Its a great clue for how long the item has been sitting on the shelf and whether another markdown is likely coming soon. If theres a lot of inventory, and its almost been six weeks since the tag was created, wait and come back next week and get it even cheaper.

Always check online vs. in-store pricing

The Home Depot website explicitly says that HomeDepot.com will not match their in-store prices, and stores do not match their online pricing.

The translation for smart shoppers is that the same item can often be cheaper depending on where you click/pay. Ive even had employees verify this over the years and they always tell me to shop one against the other, and always look for the best price.

The fastest way to stop overpaying:

When standing in an aisle at The Home Depot, pull out their app and search the exact item.

If the online price is cheaper, dont overthink it. Just buy it online, choose store pickup, and grab it on the way out and move on with your life.

Why it matters:

If Home Depot wont match their own website (and the website wont match the store), your discount is sometimes going to be simply choosing the cheaper checkout lane.

Start with Daily Deals before you pay full price

Most shoppers are not aware that Home Depot has a Daily Deals / Special Buy of the Day page that rotates deals across appliances, home dcor, and home improvement items.

This is where you should always check first when your purchase is not time critical, especially if youre not shopping for a particular brand, just the best deal.

Look for great deals on the following:

Lighting

Rugs

Storage/organization

Small appliances

Some tool bundles

Heres what the smart shopper does:

If your project can wait 4872 hours, be sure to check Daily Deals first.

If todays deals arent in the category you need, check back again tomorrow.

Home Depot literally tells you its a one-day deal setup, so the savings often comes down to timing and the ability to wait for the deal you need.

Join Pro Xtra even if youre not a Pro

Home Depots FREE Pro Xtra program is framed as a Pro loyalty program with some cool perks, promos, and the ability to track your spending.

Heres why regular shoppers should care:

Home improvement returns and price adjustments live and die by your proof of purchase. If youre doing a project over several weeks or months, that paper receipt is basically guaranteed to vanish.

Use Pro Xtra for the boring money-saver stuff:

Track purchases/spend (useful for projects and warranty claims)

Keep receipts organized instead of digging through your car console

If you dont want to sign-up for a Pro Xtra account, at least be aware that Home Depot offers the ability to look-up your receipt through your regular account.

Pro tip: If youre knee deep in a DIY project and still in the planning phase, be sure to look for quantity discounts from Home Depot before you make any purchases. You can get savings up to 20% when buying large quantities of lumber, building hardware, insulation, and even roofing materials.

Rent the expensive tool youll use once

Most Home Depot locations have a full tool and equipment rental operation. Using their tool rentals is one of the most practical save hundreds moves because buying tools for one project is how budgets explode.

Renting usually beats buying for:

Floor sanders

Pressure washers

Tile saws

Post-hole augers

Carpet cleaners

Quick decision rule (simple, not perfect):

If you wont realistically use it 23 more times, renting is often the cheaper path.

Also, renting forces you to finish the job quickly as youre getting charged by the day. This basically forces you to save money and get the job done in a timely manner.

The underrated hack: buy retired rental tools

Heres a Home Depot trick most shoppers dont even know exists. Some stores actually sell their retired rental tools at a huge discount.

That means you can sometimes get a legit brand-name tool for way less because its being cycled out of their rental fleet.

How to use this without wasting a Saturday:

Go to the stores Tool Rental area.

Ask: Do you sell retired rental tools? What do you have right now?

Inspect it like youre buying a used car:

Check the cord/battery contacts

Look for cracks, missing guards, stripped screws

Ask whats included (case, charger, accessories)

Or visit their Used Tools page on their website and enter your Zip Code to see if your local store has used tools available for purchase.

Why its worth it:

If you want to own an expensive tool but cant justify the brand new price, retired rentals can really help your budget. Think of them as cheaper than new, but way better than sketchy marketplace tool listings.

Related Bing News Results Consumer Reports |Experts warn against daily use of protein supplements Mon, 20 Oct 2025 22:57:00 GMT Protein powders and shakes are more popular than ever, often touted as workout fuel or even meal replacements. But a new Consumer Reports investigation reveals a hidden risk: some of these supplements ... A study found lead in popular protein powders. Here's why you shouldn't panic Thu, 16 Oct 2025 12:07:00 GMT A Consumer Reports investigation has found what it calls "concerning" levels of lead in roughly two dozen popular protein powder brands — but says that's not necessarily cause for tossing them. The ... Consumer Reports Is Fearmongering Again Thu, 16 Oct 2025 06:46:00 GMT We preselected all newsletters you had before unsubscribing. Your Daily Protein Shake Might Be Exposing You to Lead, Consumer Reports Finds Tue, 14 Oct 2025 03:10:00 GMT Plant-based powders, particularly those made with pea protein, were found to have the highest lead levels — and only a handful of brands were deemed safe for regular use in the nonprofit’s analysis. A ... Your Daily Protein Shake Might Be Exposing You to Lead, Consumer Reports Finds Mon, 13 Oct 2025 17:00:00 GMT A Consumer Reports investigation found that more than two-thirds of tested protein powders and shakes contained more lead per serving than what food safety experts deem safe for daily consumption.