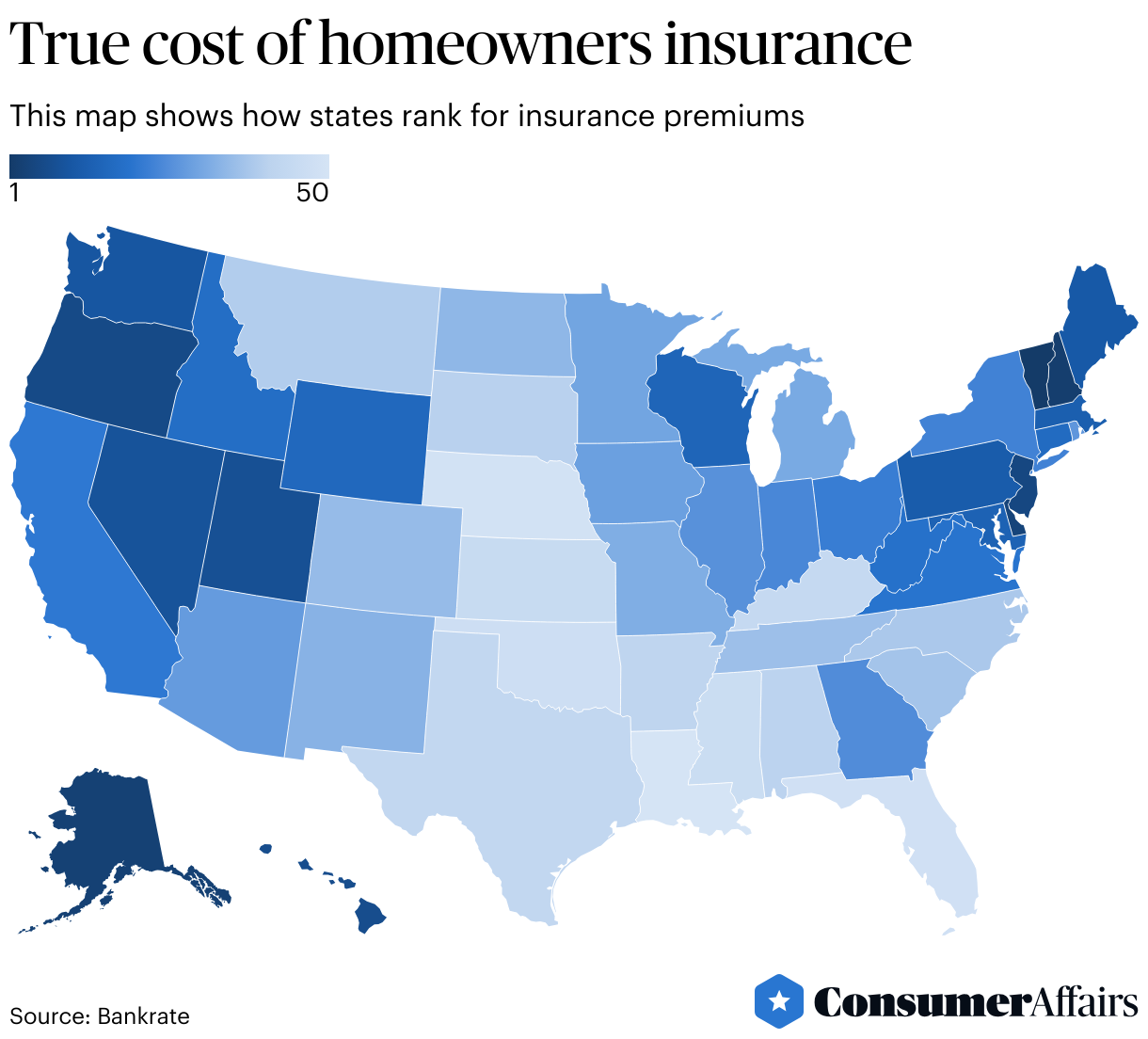

A breakdown shows states most vulnerable to disasters have the highest rates

-

U.S. households now spend an average of $2,470 a year on home insurance, or 3.18% of median household income.

-

Homeowners in Louisiana, Nebraska, and Florida face the steepest true costs, driven by extreme weather risks.

-

Since 2023, average home insurance premiums have risen 9% nationwide, outpacing income growth in many states.

Homeowners insurance costs can vary a lot, depending on where you live. Some states are more expensive because they are vulnerable to extreme weather and natural disasters.

Bankrate recently published a study, using data from Quadrant Information Services and the U.S. Census Bureau, to show where costs are highest. The study reveals that homeowners are devoting a larger share of their paychecks to insurance than ever before, with weather disasters and construction costs pushing rates higher.

On a national average, U.S. households spend $2,470 annually on homeowners' insurance, consuming 3.18% of the nations median income. Rates have climbed steadily, rising 9% since 2023. Premiums increased by $104 (4.6%) between 2023 and 2024, and another $105 (4.4%) from 2024 to 2025.

But averages only tell part of the story. Depending on where homeowners live, the true cost of coverage can vary dramatically. The map below provides a visual representation of where premiums are highest and lowest.

States with the highest true costs

Louisiana, Nebraska, and Florida rank at the bottom of Bankrates affordability index. In Louisiana, where frequent hurricanes drive up claims, the typical policy costs $6,274 10.78% of the states median household income of $58,229.

Nebraskans, vulnerable to tornadoes and hail, spend 8.61% of their income on premiums. Floridians, long plagued by high insurance costs, dedicate 7.82% of their earnings to coverage despite recent legislative reforms aimed at stabilizing the market.

The common denominator? Extreme weather. Insurance companies pass along the risks of catastrophic events in the form of higher premiums, leaving homeowners footing the bill.

Posted: 2025-08-27 11:29:44