Expert weigh in

March 5, 2026

-

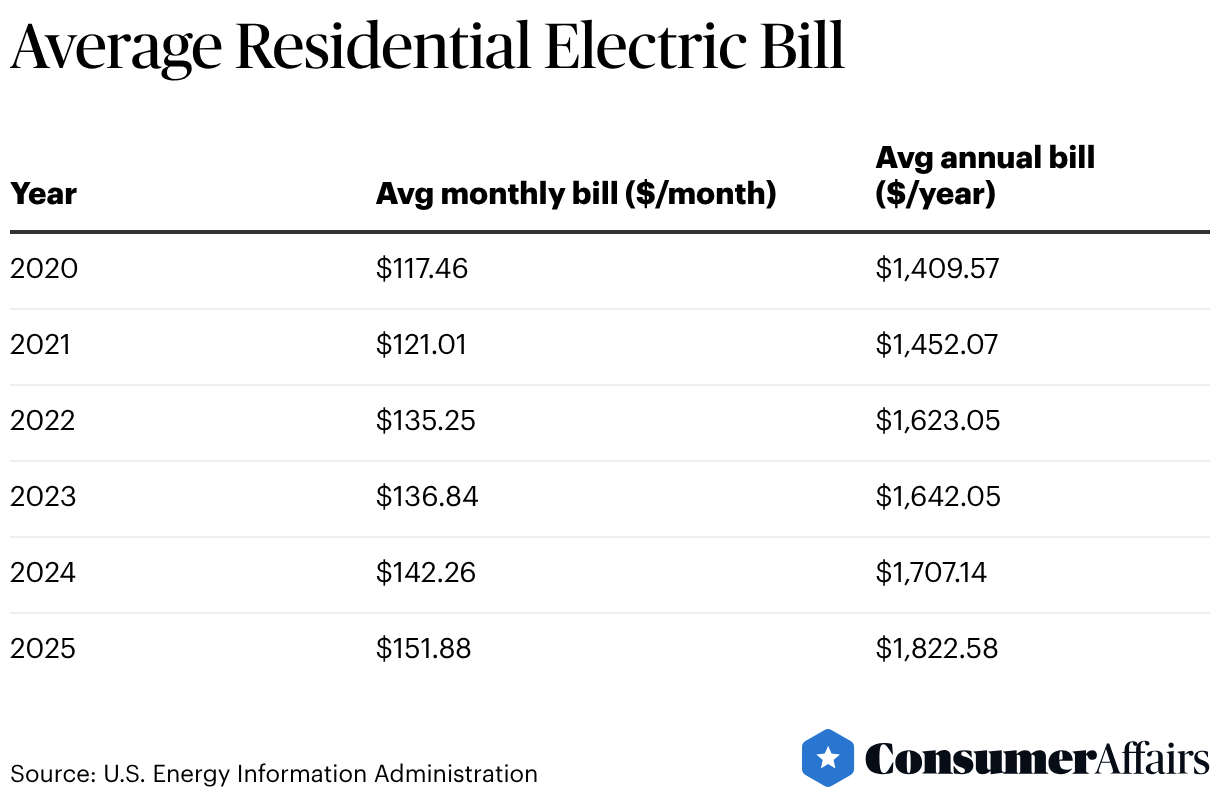

Since 2020, the average U.S. residential electric bill has increased 29.3%, as energy demand climbs with the rapid expansion of AI-powered data centers.

-

Experts say utilities are investing billions in new power generation and transmission to meet data center demand, and those costs are often spread across all ratepayers, including households.

-

Policymakers say new rate structures and requiring tech companies to fund their own power needs could help prevent residential customers from subsidizing data center electricity use.

Since 2020, residential electric bills have soared. The rising bills coincide with the rapid construction of large data centers that power artificial intelligence.

A ConsumerAffairs analysis of the Energy Information Administrations Electric Power Monthly reports found that the average residential electric bill has risen 29.3%.

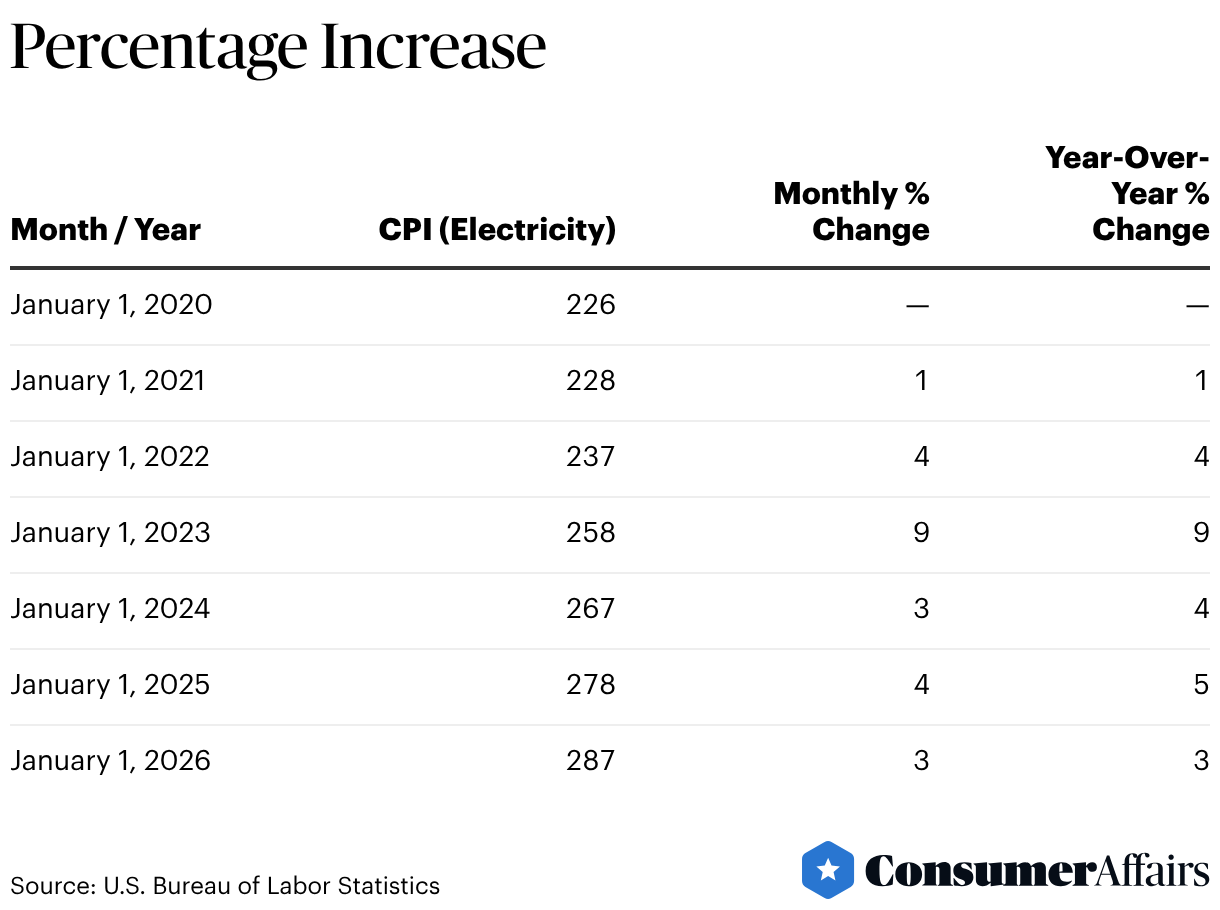

An analysis of Consumer Price Index data from the Bureau of Labor Statistics for the same years shows a similar rise, including a spike during 2022 and 2023, when inflation reached a multi-year high.

Phil Odonkor, power grid and energy sustainability expert from Stevens Institute of Technology, says its a simple matter of supply and demand.

There is not enough new power to meet the rising demand, which is hiking up prices,Odonkor told ConsumerAffairs.

Chris Black is the CEO of GridX, a company that works with utility companies on rate design for consumers. Black said data centers consume a lot of electricity and residential customers are subsidizing a lot of it. But he says data centers dont have to be the villain.

With the right rate structures things like long-term contracts, minimum demand commitments, and smarter tariff design that incentivizes data centers to flex their load during peak periods utilities can actually protect residential customers and keep bills in check, Black said. That's the direction this industry needs to move tools and rate structures that put people first, not as an afterthought."

Sudden spike

For two decades, electricity demand was relatively flat. Utility companies didnt see the need to build capacity as a rapid rate. But utilities in states with the fastest growth in data centers, bills have spiked.

In states like Virginiathe world's largest data center hubhousehold bills in some regions have already soared by 267% over the last five years as utilities scramble to keep up with the load, said Greg Field, owner of PGT Home Energy Solutions.

Arif Gasilov, partner at Gasilov Group, a firm that works on energy regulatory and sustainability strategy, says utilities are filing massive capital spending plans to serve projected loads, and those infrastructure costs get spread across all ratepayers, including residential customers.

In Nevada, for example, NV Energy's latest resource plan projects a 47% increase in electricity demand driven almost entirely by data center growth, and its Greenlink transmission project ballooned from $2.5 billion to $4.2 billion, with roughly 80% of that line's capacity committed to data center operators.

Meanwhile residential customers in the same service territory just got a new daily demand charge. The cost allocation question of whether data center operators are paying their fair share of the grid buildout they're driving, or whether residential and small commercial customers are subsidizing it, is one that utility commissions are only starting to discuss.

Fox Swim, senior solar industry researcher at Aurora Solar, agrees that the rapid buildout of AI data centers is driving a surge in electricity demand.

Expect volatile energy prices

There are an incredible number of factors that will play a role in whether energy prices change this year, most of which are not clear yet, Swim told us. Regardless of how this plays out, consumers can probably expect that energy prices will be quite volatile this year, with an overall trend upward."

National policymakers have taken notice. President Trump addressed the issue during last months State of the Union address.

Many Americans are also concerned that energy demand from AI data centers could unfairly drive up their electric utility bills, Trump said, announcing efforts to require major technology firms to provide for their own power needs when they construct data centers.

Three Senate Democrats also sent letters to seven large tech firms, calling on them to provide support for residential utility customers who are facing rising bills.