A Brief History of the Affordable Care Act

The Affordable Care Act (ACA), signed into law on March 23, 2010, was a landmark reform aimed at expanding health coverage, improving care quality, and reducing costs. It introduced:

- Subsidized insurance via marketplaces

- Medicaid expansion for low-income adults

- Protections for pre-existing conditions

- Essential health benefits like maternity care and mental health services

Despite legal challenges and political opposition, the ACA has endured and evolved. The Inflation Reduction Act of 2022 extended enhanced subsidies through 2025, contributing to record-high enrollment of over 21 million in marketplace plans.

For a detailed timeline and legal milestones, visit KFF’s ACA history overview and HHS’s official ACA page.

Real-Life Stories: The ACA’s Human Impact

Nathan’s Story – Brain Tumor Survivor

Nathan, a caregiver from Virginia, had a brain tumor he named “Fred.” Before the ACA, his insurance cost $483/month with a $5,000 deductible. After the ACA, he found a plan with a $64 premium, $850 deductible, and $10 copay for his medication. This allowed him to continue caring for clients with disabilities and live with dignity.

Gail’s Story – Cancer Survivor

Gail O’Brien was denied coverage due to cancer. Her family paid out-of-pocket for tests, and she faced draining her retirement savings for treatment. Thanks to the ACA’s Preexisting Condition Insurance Plan, she received coverage and life-saving care.

Families and Young Adults

The ACA allowed young adults to stay on their parents’ insurance until age 26, helping millions transition into adulthood with coverage. It also introduced essential health benefits like pediatric care and mental health services.

Explore more testimonials in The Stories That Saved the ACA and American Progress’s ACA legacy collection.

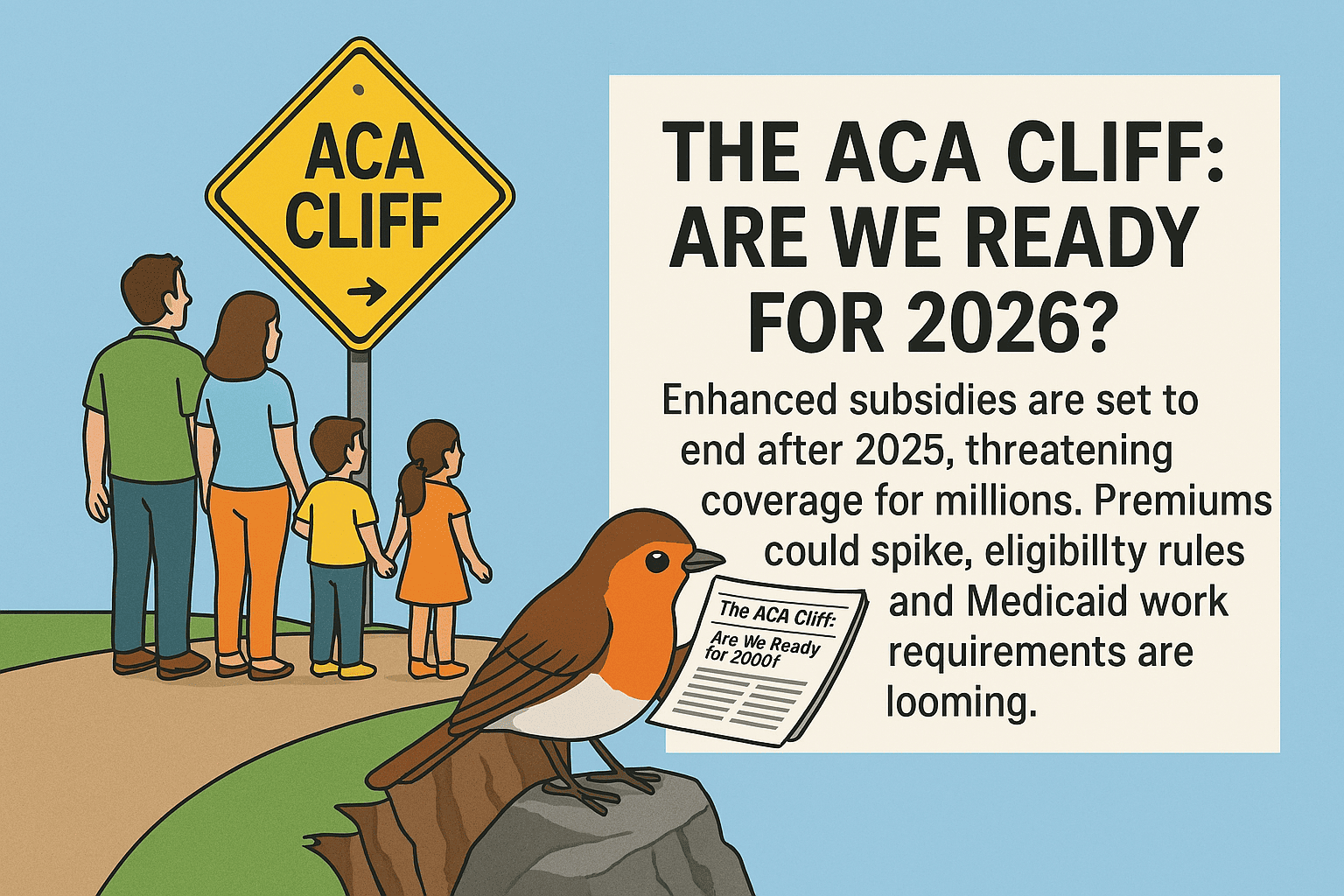

As the Affordable Care Act (ACA) approaches a point of potentially disastrous inflection, millions of Americans will soon learn a sour reality: increased premiums, reduced subsidies, and diminished eligibility. As rising federal support approaches its deadline after 2025, the health coverage landscape is about to experience a tectonic shift , which is popularly known as the "ACA Cliff".What's Changing in 2026?

Premium spikes: ACA plans are projected to rise by 18% on

average in the country.

Out-of-pocket spikes: Without subsidies, some families may

see expenses rise by 75% or higher.

Stricter eligibility: Real-time income verification will be

required; auto-renewals will lapse in 2027.

Immigration restrictions: Subsidies would only go to green

card holders and specific groups.

Medicaid work requirements: Starting in 2027, work,

volunteer, or attend school for 80 hours/month must be

accomplished by able-bodied adults.

Washington State: Get Ready for the Impact

Over 284,000 residents in Washington rely on ACA plans. The

state's Health Benefit Exchange has already approved a 10.7%

premium increase for 2025, with additional increases expected

in 2026. Insurer exits—like PacificSource and Aetna—are

minimizing choices, but Premera Blue Cross is adding a new HMO

division to fill gaps.

Local clinics and health navigators are already sounding the

alarm. “We’re preparing for a wave of uninsured patients,”

says a Bothell-based health coordinator. “If subsidies

disappear, many families will be priced out.”

What Can Be Done?

Advocacy groups are urging Congress to extend enhanced

subsidies and block restrictive Medicaid reforms. Meanwhile,

state officials are exploring policy buffers to protect

vulnerable populations.

For individuals, the message is clear:

Verify your coverage in advance.

Keep an eye out for changes in eligibility.

Contact your legislators to fight for ACA protections.

Call to Action

The ACA Cliff is not a matter of policy debate; it's a looming crisis facing working families, seniors, and small business owners. RobinsPost.com encourages readers to speak up, remain vigilant, and prepare for the changes that are headed our way.